Chapter 58

Real Estate Arithmetic and Mathematics

Real estate practitioners perform many types of calculations. These calculations are more arithmetic than mathematics. Arithmetic deals with real numbers and the manipulation of these numbers. These real numbers include decimals and fractions. The manipulation of these real numbers involves the four functions of addition, subtraction, multiplication and division. Mathematics goes beyond artithmetic with concepts like geometry, algebra, etc. The calculations in real estate entail a little bit of geometry when dealing with square feet of a site or structure.

The basic presumption in this chapter is that the reader has a firm grasp of decimals and fractions and their manipulations. Given existing educational curricula these arithmetic concepts are taught in grades one through six in most school systems. For this reason this chapter does not include a review of decimal and fraction arithmetic. If the reader needs a review of these concepts there are several books on the market typically entitled “real estate mathematics” that provide such a review.

Specifically, real estate arithmetic in this chapter consists of the following calculations:

- Commission Calculation

- Sales price to list price ratio

- Interest payments or receipts

- Discount points and origination fees

- Appreciation and depreciation

- Real Property taxes

- Proration

- Area measurements

These topics appear in the following sections of this chapter. The order of their presentation does not signify any opinion about their relative importance.

In addition to these concepts real estate arithmetic also includes the following calculations that are handled in other chapters.

- Mortgage math

- Qualifying the Borrower

- Appraisal math

- Investment analysis

- Closing or settlement statements

- Compound interest (six functions of the dollar)

Commission Calculation

Commission rates are expressed as a percentage of the sales price. A specific commission rate, such as 5%, is not set by law, nor should it be set by custom or tradition. According to the federal government, commission rates are negotiable. In the past, brokers have been sued by the federal government for price-fixing as a violation of the Sherman Anti-Trust Act, with regard to collaboratively setting real estate commissions in their local market areas.

The arithmetic involved in commissions is the application of a negotiated commission rate (a percentage) to the sales price of property. Sales price times the commission rate equals the commission. For example, if the negotiated commission is 5%, and the property sells for $200,000, the commission is $10,000.

Sales Price x Commission Rate = Commission

Illustrative problem #1:

A property sells for $187,500 and the commission rate is 6.25%.

What is the commission?

$187, 500 x 6.25% = $11,718.75

Illustrative problem #2:

A property sells for $212,450 and the commission rate is 5.85%.

What is the commission?

$212,450 x 5.85% = $12,428.33

Commission Splits

When a real estate transaction involves 2 brokers working on a co-brokered or co-oped deal, commissions are typically split between the listing broker and the selling broker; for example, this could be a 50%/50% split, or as negotiated between the brokers. So, a $10,000 commission would be split $5,000 to each broker. Often, the $5,000 commission that went to each brokerage is further split between the broker and the sales associate. Here the split can vary based on many variables, and will be documented in a written agreement between the brokerage and the associate. For example, if the split is 60%/40% to the broker, the broker gets $3,000 ($5,000 times 60%) and the sales associate gets $2,000 ($5,000 times 40%).

Sales price to list price ratio

Brokers and sales associates who list a property will price the property, in consultation with the seller, so that the property sells in a reasonable amount of time with adequate market exposure. This is traditionally done using a comparative market analysis, or CMA. (Note: this process is not an appraisal.) Then to provide room for negotiation, the list price is set above that anticipated sales price. If the anticipated sales price is $150,000, the list price might be set at $160,000. If the property actually sells for $154,000, the sales price to list price ratio is 96.25% ($154,000 / $160,000).

Simple interest payment

A simple interest payment is calculated as the amount of the loan times the interest rate on that loan. For example if the loan amount is $150,000 and the contract interest rate on that loan is 6% per year, the simple interest for the first year of the loan is $ 9,000

Loan amount x interest rate = interest payment

Illustrative problem #1:

A buyer borrows $140,000 at the contract interest rate of 8.25%.

What is the borrower’s total interest payment in the first year?

$140,000 x 8.25% = $11,550

Illustrative problem #2:

A lender provides a $215,475 loan to a borrower at a contract interest rate of 6 3/8%.

How much interest does the lender receive in the first year?

3/8 equals 0.375

$215,475 x 6.375% = $13,736.53

Illustrative problem #3:

A lender receives a $9,654.12 interest payment in the first year on a 6% loan that he made to the borrower. What is the loan amount?

Loan Amount x Interest Rate = Interest Payment

Loan Amount = Interest Payment / Interest Rate

Loan Amount = $9,654.12 / 6%

Loan Amount = $160,902

Discount points and origination fees

Discount points and origination fees are front-end charges that may be imposed by the lender when making a loan. The lender uses discount points to increase his rate of return on the front end without raising the interest rate over the life of the loan, which would raise the monthly payment for the borrower. The lender charges loan origination fees to cover the costs associated with data gathering and evaluation of the borrower’s financial ability to repay the loan amount. One discount point is equal to 1% of the loan amount. An origination fee may also be stated as a percentage of the loan.

With regard to discount points the explicit wording of the loan agreement dictates how the points are to be paid. If the statement says “a loan in the amount of $100,000 at 5% for 30 years plus 2 discount points” the word plus indicates payment of the points at the time the loan is issued. For example, a loan of $100,000 at 5% for 30 years plus 2 discount points requires a payment of $2,000 for discount points ($100,000 x 2% = $2,000) at the time of the loan closing.

Points paid up front increase the amount of funds the borrower requires to close. This may be a trade-off for keeping his monthly payment lower, which may even allow the borrower to qualify for the loan that he may not have qualified for at a higher monthly payment. If the price of the property is $120,000 and the loan amount is $100,000, the borrower must come to the closing with the $20,000 down payment, plus the $2,000 in points to close the loan.

In some situations the discount points are netted out of the loan. For example, a loan of $100,000 at 5% for 30 years with2 discount points requires a payment of $2,000 for discount points ($100,000 x 2% = $2,000). But, in this situation, the borrower signs the promissory note to repay $100,000, but the dollar value of the discount points is subtracted out of the proceeds, and the borrower receives a net disbursement of $98,000. The operative word in this transaction is “with”, vs. “plus.”

Origination fees are often expressed as a percentage of the loan amount. For example, a loan amount of $120,000 with a 1% loan origination fee, generates an origination fee of $1,200. This should be considered an additional cost of financing.

Appreciation and depreciation

Appreciation is an increase in the value of a property. For example, several years ago the property was worth $120,000; today it is worth $150,000. Over time the property appreciated by $30,000. On a percentage basis, this is a 25% appreciation over the time. This is calculated as $150,000 – $120,000 = $30,000. $30,000 / $120,000 = 25%) If the time period is 10 years, this is a simple annual appreciation rate of 2.5%.

In practice historical appreciation rates are often used to look forward in time for real estate investment analysis. An analyst might consider the historic appreciation rate in a market for a specific type of property and use that as a basis to predict future values. For example, a property is currently worth $200,000 and the historic appreciation rate has been 2% per year for the previous five years. What is the property worth five years in the future? Using the simple annual average of 2% for five years equals the total appreciation of 10%, so the property would be projected to be worth $220,000. Analysts will often use a compound appreciation rate which will be discussed in the later section of this chapter. When a 2% compounded appreciation rate per year is used, the current $200,000 property would be projected to increase in value to $220,816.

Depreciation is a decrease in the value of a property. For example, several years ago, a property was worth $150,000; today it is worth $120,000. Over time, the property depreciated by $30,000. On a percentage basis this is a 20% depreciation over time. This is calculated as $150,000 – $120,000 = $30,000. $30,000 / $150,000 = 20%. If the time period is 10 years, this is a simple annual depreciation rate of 2%.

Like the appreciation rate, the depreciation rate can be used to project the expected future value of a property.

Real estate taxes and millage rates

Real estate taxes are based upon the market value of the property as determined by the city or county jurisdiction in which the property exists. In the year of sale, the market value of the property may be presumed to be the sales price of the property. In subsequent years after sale, the tax assessor of the jurisdiction estimaates the fair market value.

Georgia uses an “assessment rate” of 40% of the market value to calculate the assessed value of the property. For example, a property’s sale price is $200,000; the 40% assessment rate of 40% generates an assessed value of $80,000. The $80,000 times the millage rate which is defined below establishes the property tax bill.

Real property taxes are a major source of income for local and state governments. These property tax revenues provide government services to a specific jurisdiction. Property tax revenues typically pay for local government personnel services (safety, teachers, judicial and administrative), equipment purchases and maintenance, infrastructure maintenance and construction, and general supplies and materials.

The property tax calculation involves a series of related actions. The first is the determination of the local budget, the sum of all funds required to cover the expenses. Assume that a budget planning process determines that the local government needs $1 million to operate in the coming year. Secondly and simultaneously, the tax assessor of the jurisdiction determines the total value of all real property (residential, retail, office, industrial, agricultural and undeveloped raw land) is worth $20 million. This is called the tax base.

The third step in the process is the calculation of an assessed value for the property from its fair market value. This is accomplished by multiplying market value by an assessment rate. In Georgia, the assessment rate is 40% of the market value. Market value x 40% = Assessed value. For example, a property worth $200,000 in the market has an assessed value of $80,000. $200,000 x 40% = $80,000

The fourth step in Georgia is the calculation of the millage rate. The tax base of $20 million is multiplied by the assessment rate of 40% to obtain the total assessed value of $8 million ($20,000,000 times 40%). These values yield a tax rate of 12.5%. (1M / 8M). The tax rate may be expressed as a percentage, but it is often expressed as a Millage rate. The millage rate is based on a 1000 instead of a 100.

1M/8M = 0.125 = 12.5% or 125 per 1000

The last step is to calculate the individual property tax for a specific property. Having calculated the assessed value, the tax rate is applied to each property in the jurisdiction. For example, assume an equalization rate of 40% and a millage rate of 125, what is the property tax bill on a property whose current fair market value is $200,000?

$200,000 x 40% = $80,000 assessed value

$80,000 assessed value times 125 per 1000 = $80 times 125 = $10,015.63

Outside of GA, some jurisdictions may calculate a different millage rate for each of the property types.

Illustrative problem #1:

In a city that has a millage rate of 60 what is the property tax on a house with the current market value of $155,000?

$155,000 x 60/1000 = $930

Illustrative problem #2:

In a city that has a millage rate of 30 mills and an assessment rate of 100% what is the property tax on a house with the current market value of $220,000?

$220,000 x 30/1000 = $6,600

If you have the real estate tax bill for a property, use the values in hand for calculating prorations. If you want to project the future tax bill for a buyer, calculate the projected real estate taxes based on the purchase price.

Proration

As part of the closing process, there are expenses and income to ownership such as prepaid or unpaid taxes, rent receipts on income property, and insurance that must be divided between the seller and buyer so that each party only pays for the expenses incurred or receives the income earned during the time that he or she actually owned the property. Proration deals with allocating these items between the buyer and the seller. An important element of this allocation is knowledge about whether the payment is “in advance” or “in arrears”. Typically, property tax is paid in arrears, with a tax bill for a current year being due in the last quarter on that year. For state testing purposes, taxes are assumed to be paid July 1, so that taxes are paid half in arrears and half in advance, spanning the period from January 1 through December 31. Property insurance and rent receipts are payments in advance.

Proration for payments “in arrears”:

Property Tax: Consider a property tax payment situation. Property tax payments are due on December 31 for the current year. Property taxes are $5,000 for the year. The property is sold on June 30. The owner and seller of the property used the property for six months, sold it, and the buyer owns it for the remaining six months in the year. The proration of property tax payment in this situation requires the seller to compensate the buyer $2,500, as the buyer will pay the entire tax bill on December 31. In this simple example, the seller owned the property for half a year and the buyer owned the property for half a year, so the $5,000 is prorated between the two of them.

(Annual Tax Bill / 365) x days in the proration period = Proration $

Consider the following illustrations of more complicated tax proration.

Illustration #1:

Property tax payments are due on December 31 for the fiscal year. Property taxes are $4,800 per year. The property is sold on April 30. What is the proration?

The seller owns the property for 120 days (Jan = 31; Feb= 28, March = 31; April = 30) while the buyer owns the property for the rest of the year, which is 245 days.. The seller needs to compensate the buyer, as he will pay the entire year’s tax bill on December 31.

$4,800/365 = $13.15 tax per day

$13.15 x 120 days = $1,578 seller to buyer proration

Illustration #2:

Property tax payments are due on December 31 for the year. Property taxes are $4,800 per year. , The closing is August 15. What is the proration?

The seller owns the property for 227days, (count days in Jan, Feb, March, April, May, June, July, and 15 days into August) while the buyer owns the property for 138 days for a total of 365 days in the year. The seller needs to compensate the buyer.

$4,800/365 = $13.15 tax per day

$13.15 x 227 days = $2,985.05 tax proration, seller to buyer

Illustration #3:

The property tax payment is due on November 1 for the fiscal year. Property taxes are $6,400 per year. The closing is November 10. What is the proration? The seller just paid the tax bill for the entire year, including the 10 months + 10 days he owned the property, and the rest of the year, that the buyer will own the property through to December 31 when the tax year ends. November has 30 days. The buyer owns the property 20 of those days, plus the 31 in December, for a total of 51 days in the tax year. The buyer needs to compensate the seller.

$6,400/365 = $17.53 tax per day

$17.53 X 51 days = $894.03 buyer to seller tax proration

Accrued Interest: Accrued interest payments occur at the closing when the seller has a mortgage payment that was paid on the first day of the month and the closing occurs during the month with the buyer assuming the loan. For example, the interest payment for the month is $900 paid in advance and the closing is on the 20th of the month. The buyer owes the seller 10 days of interest. The amount of the proration is $900 divided by 30 days = $30 per day times 10 days yielding $300 as the proration.

Proration of payments “in advance”

Insurance: Property insurance is paid in advance. However, in most cases the buyer obtains his or her own property insurance and proration of insurance payment is not an issue at closing. If the buyer accepts or assumes the seller’s property insurance, the proration process involves reimbursing the seller for the prepaid insurance premiums. The proration is for any 365 day period. So, one must determine the starting and ending dates of the policy, and calculate how many days of the policy period the seller has used while owning the property, and how many the buyer will use until the end of the policy period. Then the buyer must reimburse the seller for the pre-paid insurance amount that the buyer will use. Here is an example:

You have a closing July 26. The buyer will be assuming the seller’s homeowner’s insurance policy, on which coverage began October 20. The annual premium is $2,690. What is the insurance proration?

The seller will receive a refund for $626.44. The insurance bill is paid in advance for 365 days starting Oct 20, and ending Oct 19 the following year. Buyer will use the remainder of the policy period after closing day July 26. That is 5 days in July, plus August, Sept, and 19 days in Oct, or a total of 85 days.

Proration calculation is $2,690/ 365 days X 85 days = $626.44

Rent: Rents are also paid in advance and typically on a monthly basis. The owner of an income property receives rent payments on the first of the month every month during the fiscal year. If the owner received $5,000 in monthly rents for the apartments or retail space and then sells the property on the 12th day of the month, proration must take place for the income, so that it is divided between the buyer and the seller according to their ownership dates. The seller must compensate the buyer. For example, the owner/seller owns the property for 12 days in April while the buyer owns the property for 18 days or a total of 30 days in the month of April. The seller must provide 18 days of rental income to the buyer.

$5,000 times (18/30) = $3,000

Pre-paid Interest: Pre-paid interest occurs at the closing when the buyer/borrower must pay for the use of the new loan amount from the closing date to the end of the month. If the closing is on March 15 the first mortgage payment is generally scheduled for May 1. This timing makes sense when you realize that mortgage payments are customarily paid in arrears in Georgia. The May 1 payment covers April. The borrower owes the interest for March 15 to March 30; this is the pre-paid interest. If the loan amount is $100,000 at 5% per annum, the interest payment is $5000 for the first year. The pre-paid interest is $5000 divided by 360 equaling $13.89 per day times 15 days yielding $208.33 for the pre-paid interest.

Transfer Tax

At the closing the property ownership transfers from the seller to the buyer, from the grantor to the grantee. The county taxes this transfer. The formula for the transfer tax is:

(Sales Price – Assumed Debt) times 0.1%

This formula simplifies to:

(Sales Price – Assumed Debt) / 1000 = Transfer Tax

For example, consider a property sale at $200,000 with no loan assumption. What is the transfer tax payment?

$200,000 / 1000 = $200

In other words, the transfer tax is currently $1 per each $1000 of sales price.

What is the transfer tax payment if the transfer tax rate increases? Consider a property sale at $200,000 with no loan assumption. What is the transfer tax payment if the transfer tax rate is $2/$1000? Intuitively, it is twice what it is a $1/$1000 which would be $400. If the tax increases to $1.50 / $1000, it is 1.5 times the amount which is $300. Arithmetically the formula should be written as:

(Sales Price – Assumed Debt) / (1000/T) = Transfer Tax

Where T is the transfer tax rate.

Intangible Recording Tax

As expressed by the Georgia Department of Revenue, an intangible recording tax is due and payable on each instrument (security deed) securing one or more long-term notes at the rate of $1.50 per each $500.00 or fraction thereof of the face amount of all notes secured thereby in accordance with O.C.G.A. Section 48-6-61 (www.gabar.org/public/pdf/SECTIONS/…/TitleStandards.pdf). This tax is assessed on the security instrument securing one or more long-term notes secured by real property, to be paid upon the recording thereof, and must be paid within 90 days from the date of the instrument executed to secure the note or notes. The maximum tax on a single security instrument is $25,000. Authority O.C.G.A. Secs. 48-2-12, 48-6.61.

For example, if the security deed and the accompanying note are for a $200,000 loan, the formula for the intangible tax is:

($ Loan/500) times $1.50 = tax

($200,000/500) x $150 = $400 x $150 = $600

Several exemptions from payment of the intangible recording tax are provided by Georgia and federal law. The Georgia Department Revenue has interpreted applicable statutes concerning exemptions in the department’s Rules and Regulations (Chapter 560-11-8-.14),

The lender can pass this tax on to the borrower.

Area measurement

Area measurement occurs for sites and structures. First consider sites.

Area measurement of sites requires a little knowledge of basic geometry. In the vast majority of situations, knowledge of the calculation procedure for a rectangle and for a triangle will be sufficient. For a rectangle you need to know length times width. A square is a special case of a rectangle, with all sides being equal. For a triangle, you need to know base times height.

A convention used in the real estate industry is to specify the width of the property along the street or road first. This measurement is known as frontage. Consider a rectangle that is 120′ x 180′. The area of this site is 21,600 square feet. This can be converted to acres by remembering that an acre contains 43,560 square feet; the acreage of this site is 0.496 acres.

120’ x 180’ = 21,600 sq ft

21,600 = .496 acres

43,560

Consider a site that is 225′ x 410′. Calculate the following measurements.

What is the frontage? Answer 225 feet.

What is the square footage of the site? Answer 225 x 410 =92,250 sq ft

What is the acreage of the site? Answer 92,250/43,560 = 2.12 acres.

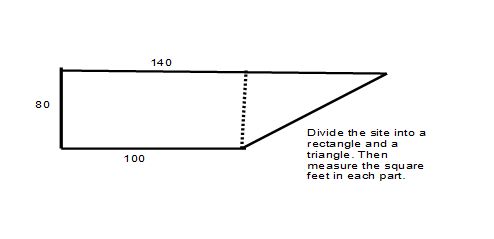

Consider the area in the chart above.

What is the frontage? Answer 100 feet.

What is the square footage?

Answer: to obtain the square footage the site needs to be divided into a rectangle and a triangle. The rectangle is 100 feet times 80 feet equals 8000 sq ft The triangle has a base of 40 feet and a height of 80 feet; the area is “one half times the base times the height of” which is (1/2) times 40×80 = 1600 sq ft. The square footage is 8000 + 1600 = 9600 sq ft.

What is the acreage? Answer 9,600/43,560 = 0.22 acres.

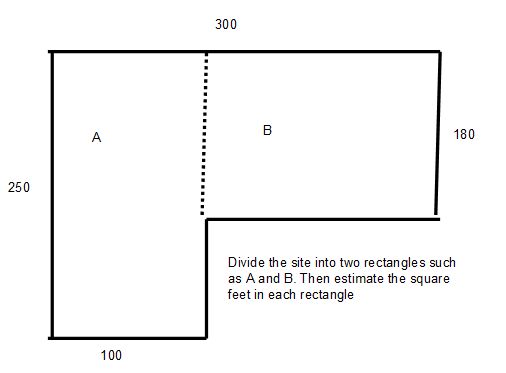

Consider the site in the chart below.

Part A is 100 feet times 250 feet = 25,000 sq ft

Part B is 200 feet times 180 feet = 36,000 sq ft

Total square footage = 61,000 sq ft

Total acreage = 61,000 / 43,560 = 1.4 acres

More complex site shapes can exist. For example in a residential subdivision cul-de-sac sites have slightly curved frontage and it irregular sidelines and back lines. Raw land or agricultural land can have frontage along a winding road and could have sidelines and/or back lines determined by a river or a stream. In such situations the estimation of square footage and acreage will require the work of an expert, most likely a surveyor.

Area measurement also occurs for structures. Structures are typically composed of rectangles, and in many instances these rectangles are stacked to form two-story houses, two-level regional malls and office buildings. So, you can calculate one level and multiply by the number of levels to obtain the total square feet.

The different property types have different area measurement definitions.

- Single-family detached houses use “gross living area”

- Retail properties use “gross building area” and “gross leasable area”.

- Office buildings use “gross building area”, “rentable area” and “usable area”.

Gross Building Area

Several definitions of gross building area exist. The first one comes from the FNMA Guidelines, Chapter 4, Section 405.7 and focuses on residences.

- Gross building area, which is the total finished area (including any interior common areas, such as stairways and hallways) of the improvements based on exterior measurements, is the most common comparison for two- to four-family properties. The gross building area must be consistently developed for the subject property and all comparables that the appraiser uses. It should include all finished above- and below-grade living areas, counting all interior common areas (such as stairways, hallways, storage rooms, etc.), but not counting exterior common areas (such as open stairways).

The second definition of gross building area comes from InvestorWords.com

- The sum of areas at all floor levels, including the basement, mezzanine, and penthouses included in the principal outside faces of the exterior walls without allowing for architectural setbacks or projections.

The third definition comes from the Appraisal Institute:

- Total floor area of a building, excluding unenclosed areas, measured from the exterior of the walls of the above-grade area. This includes mezzanines and basements if and when typically included in the region. Source: Appraisal Institute, The Dictionary of Real Estate Appraisal, 5th ed. (Chicago: Appraisal Institute, 2010).

Also see the many industry definitions prepared and sold by the Building Owner and Managers Association (BOMA) (http://www.boma.org/MeasurementStandards)

Closing exercises

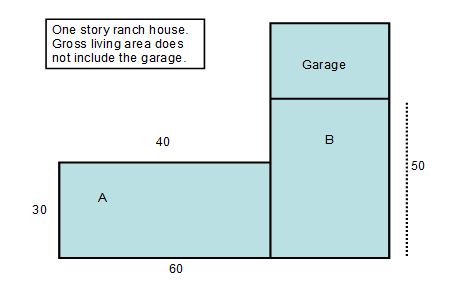

Consider the following single family residential structures (see chart below):

Part A 40’ x 30 = 1200’

Part B 20’ x 50 = 1000’

What is the gross living area of the house? Answer: 2,200 square feet

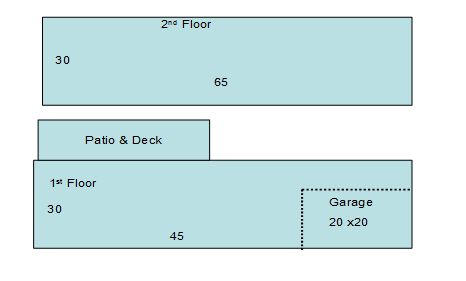

Consider the following chart below.

1st Story (45’ x 30’) + (20’ x 10’) = 1,350 + 200 = 1,550

2nd Story 65’ x 30’ = 1,950

What is the gross living area of the house? Answer: 3,500 square feet